If you want to build your wealth, you need to save money and invest. But where should you put more of your effort? In this article, you will know why your savings rate is more important than your rate of return.

During your early years of saving for financial independence, the savings rate is your most important number. Sure, having a high rate of return is fun, but it shouldn’t be your priority. After you have some leverage in the form of thousands of dollars, your rate of return comes in.

This means that you need to save rather than think about and prioritize your returns. Do you know why? Because you cannot control your returns.

Especially when you invest your money, there are certain risks that can affect your returns. This is always a possibility, so you need to consider risk all the time.

Do you want to understand this more? Then look no further and get to know my friend Dave as an example.

The Story Of Dave

Dave keeps talking and talking about his cryptocurrencies. He checks his portfolio every day, where he shares what his year-to-date return is. Dave bought a lot of crypto’s when the market was low throughout the year, for around $1000. Now his portfolio has a value of $1500 within a year. That’s a 50% increase in only one year. Talk about beating the market!

I know how Dave is wired. We talk about how we’re going to retire early and save most of our income. He’s very interested in personal finance. His habits are different from mine, though.

He plans to buy new shoes, clothes, an Xbox, and a Macbook every time he gets his paycheck. He’s setting aside $80 per month for his cryptocurrency investments, which after a year grew to $1500.

50% Return On Nothing – Still Nothing

In his mind, he’s killing it, and his cryptocurrencies will for sure enable him to retire before 45. Of course, a 50% return on investment in one year is impressive.

He’s outperforming the market and doing a great job.

He turned his $1000 investment into $1500 in a year’s time. If my investments did that, my time to retirement would be a lot shorter.

The point is that he thinks that this monthly $80 in cryptocurrencies will be able to retire him at 35. While I love his determination, I also think there should be a realistic plan on the table for how you’re going to accomplish retirement.

If he’s putting money aside for a year and has saved $1500 until now – it’s not really moving the needle. I didn’t ask if he had any specific retirement number, but $1500 isn’t going to be enough for anyone.

We want dollars. Thousands and thousands of them. Preferably even more.

How are we going to do that? We’re going to save a big percentage of our income from getting a lot of money in our savings and investment accounts.

Big Returns Are Sexy

New investors often look at big returns. Big returns are sexy, and they give you the feeling that you’ve received ‘free money.’ While big returns are every investor’s dream, it’s not something that you should focus on at the beginning of your journey.

If you’re a new investor and have $1000 invested, will the rate of return make a big impact? For a 50% return on investment, you ‘only’ gain $500. What if he would have saved 50% of his income, and he would have $10,000 in the bank. His investments would need a 5% increase to have the same absolute gain.

While big returns are sexy, it’s important first to build up your investment portfolio. Once you’ve built up your investment portfolio, your rate of return will start having some impact.

Compounding Without Anything To Compound

“Compounding interest is the eighth wonder of the world. He who understands it earns it. He who doesn’t pays it” – Albert Einstein.

Compounding interest is awesome. It means that your returns are also generating. When you’re, for example, having $10 that doubles every day for two weeks, you get the following results:

Day 1: $10

Day 2: $20

Day 3: $40

Day 4: $80

Day 5: $160

Day 6: $320

Day 7: $640

Day 8: $1,280

Day 9: $2,560

Day 10: $5,120

Day 11: $10,240

Day 12: $20,480

Day 13: $40,960

Day 14: $81,920

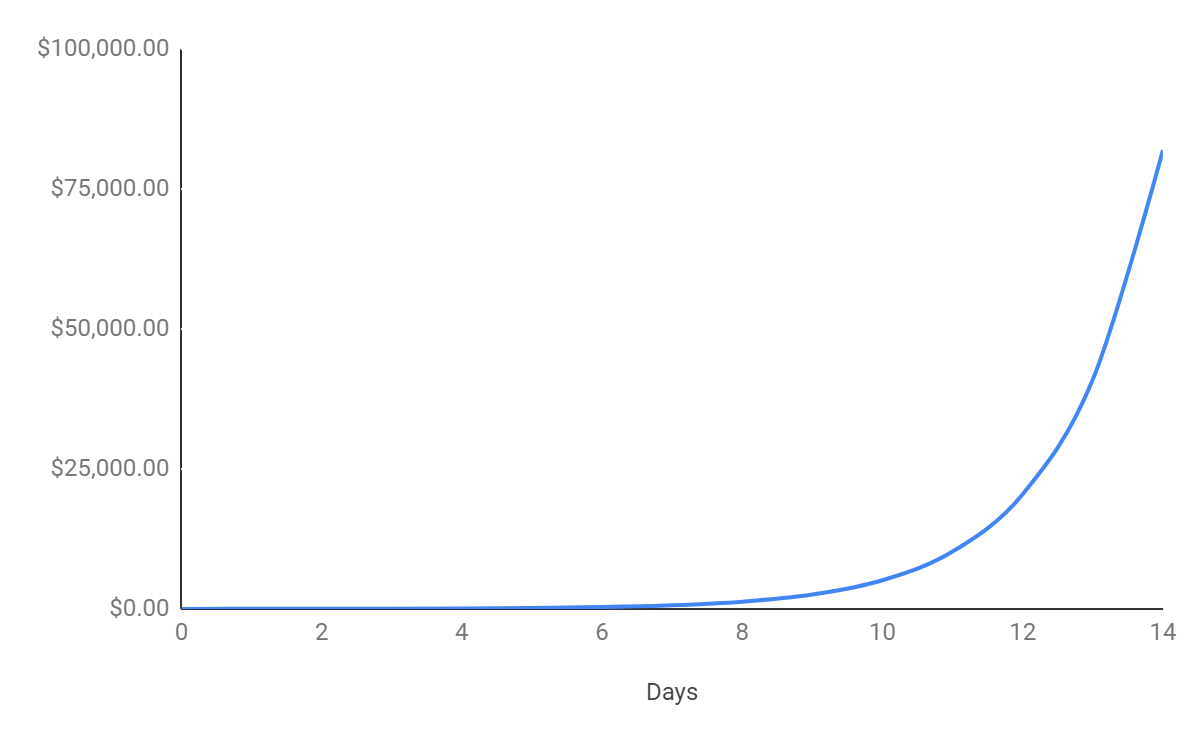

Let’s Make It Visual

When we put this into a graph, you get the following visual representation:

This example illustrates compound interest and its returns. When you double the $10 for only two weeks, you already have $81,920.

When you double a penny for 30 days, you even get to over $10 million!

While compounding interest is great, it might focus on the wrong things early in the game. When your investment amount is not so big yet, increasing the principal amount is more important.

If you look at the example early in the day, compounding doesn’t have as much effect. $20 becomes $40, that’s it.

You can see that most of the growth happens in the last few days when there is already a significant amount saved. That means instead of focusing on the rate of return, we should only focus on our savings rate at the beginning of the game. The savings rate is the only number you can influence – put as much money away so that you can get to those big numbers earlier.

The only way to get to compounding significant numbers over time is by saving as much as you can to get to the bigger numbers as soon as possible. That’s basically how I’m approaching financial independence, by focusing on my savings rate.

How To Get To Those Numbers?

First, let’s talk about how to calculate your savings rate. I calculate it as the Amount Saved divided by Net Income.

Now, let’s look at steps you can take to increase your savings rate. You must set up a budget that fits you. A budget has this reputation of being restrictive, which I disagree with. A budget is a way to prioritize the things that are important to you. Saving money can be fun and exciting! Anyways, if you’re not the budget type, you can simply pay yourself first.

I’ve also listed how I save over 50% of my income, and you can too!

Besides saving more money, you can also make more money. A lot of people underestimate the importance of your career in the whole picture. If you’re getting consistent raises over a specific time, the compounding effect will also kick in. Not sure how to get a raise? Read more about it here. After one year of working, I got a 20% raise, so I’m giving you my tips and tricks to get the same thing done yourself!

Besides all of this, I received some great money lessons from my dad when I was young. You can read more about them here.

Focus On Things You Can Control

I’ve read Seven Habits of Highly Effective People, which is truly a great book, and I would recommend it to all of you. They speak about this circle of control and circle of influence.

Seven Habits of Highly Effective People says that you should only focus on the circle of your control. When you focus on the circle of concern, you’re wasting your energy on this you can’t change. Because you’re wasting your energy on the circle of concern, the circle of control will get smaller – as less energy is directed there.

What I’m trying to say is: focus on things you can control.

Maximize Your Savings And Return

As I’ve mentioned earlier, it is best to focus first on saving when building your wealth. This means it is best to put effort into your savings rate while you are still in the early stages of increasing your nest egg. You may do that by doing side hustles aside from your normal day job.

As your financial journey continues, you may now give importance to your investments. You need to make sure that you do your research and conduct due diligence with your investments. During this time, you need to protect them from losses by improving your portfolio. You become more sensible with your investments when you try to grow your money.

This means that you also need to invest to maximize and reach your financial goals over time. As you become more experienced with investments, you will consider what risks you can take to get the returns you want.

As your savings rate is pretty much secure already, you have some leeway to take some risks through investments.

Try M1 Finance for your investment needs. Check out our full M1 Finance review to learn more about the services and start investing for free.

In Summary: Your Savings Rate Is More Important Than Your Rate Of Return

Your savings rate is something you can control. Your rate of return is something that is out of your hands. Of course, you can invest in peer-to-peer lending to get a fixed rate of return, but also that is beyond your influence. As soon as you have put your money on the platform, it’s not in your control anymore.

Sure, it’s fun to have a rate of return of 50% yearly and make $500 on that. Will it change your path to retirement? Probably not. You need a significant amount of money first. Your rate of return will get more important once you have a lot of money saved.

10% return on $300,000 is $30,000 per year, which will have a big influence.

That’s why your savings rate is more important than your rate of return, particularly at the beginning of your journey.

It’s like building your house. Your savings should be your foundation since this should be strong, solid, and stable.

From there, you can build up your house through your investments. Having this formula will help you weather any challenge that comes your way.

Do you focus on your savings rate or your rate of return?

Founder of Spark Nomad, Radical FIRE, Journalist

Expertise: Personal finance and travel content

Education: Bachelor of Economics at Radboud University, Master in Finance at Radboud University, Minor in Economics at Chapman University.

Over 200 articles, essays, and short stories published across the web.

Experience: Marjolein is a journalist and founder of Radical FIRE, a personal finance platform, and Spark Nomad, a travel platform. Marjolein has a finance and economics background with a master’s in Finance. She has quit her job to travel the world, documenting her travels on Spark Nomad to help people plan their travels. Marjolein has written for publications like MSN, Associated Press, CNBC, Town News syndicate, and more.

Thanks Josef!

Really informative! Looking forward to more updates on this.

Saving madly is step one, and getting a good rate of return for your money is step two. Lots of people skip to step two, while step one is often forgotten. It’s great that you’re focusing on both! 8% is always better than the percentage that you get in your bank account. If you’re already saving a good amount of money, then it gets important how much return on investment you’re getting

“I think that they focus on making a quick high return rather than investing for the long term in an index fund which will give them a better and more reliable result.” – I couldn’t agree more! That’s part of the problem, where people are only focusing on the quick buck rather than on the long term game.

I think that I do both – saving madly to increase the money that I have to invest, but also trying to get a good rate of return. For me though that is a stocks and shares ISA (tax-free UK savings account). At the moment my index fund is returning 8%, which compared to where I had my money previously, in a bank savings account at 1%, is a great return for me, as well as spreading the risk. Speaking to others I think that they focus on making a quick high return rather than investing for the long term in an index fund which will give them a better and more reliable result. As always, people want a quick fix rather than being prepared to wait.

Thanks Nate! Getting into the habit is important indeed, only Dave is only focusing on crypto’s and he doesn’t want to invest in index funds. He’s only better on crypto’s going x200 over the longer term. Well at least he’s investing for the long term lol. Once you’ve got that monthly savings covered, increasing your savings can really speed up your way to any financial goal. Great that you’re already doing that, I’m sure it will pay off on the long term!

Hi Emil! I agree, the first step to investing is saving money to actually invest. Actually being patient and waiting is hard for a lot of people, good thing you got that covered. Glad you enjoyed the post!

So true, great post!

I do understand where Dave is at. When you are first getting started saving even small dollars do matter just to get in the habit of saving. I hope that this Dave is also diversifying into index funds!

But you are right, as you go you need to ramp up your savings rate. Personally, every time I get a raise or a bonus I increase the deferral rate in my 401(k).

Yes, this is the first step to invest:save

The more the better.

Regarding bitcoin. It’s to volatile. Every up follows an down and viceversa. Gold is king. Of course on a long term.

For anything else you have to wait and patience. I am like a fisherman when you wait for the big one.

I don’t know. Maybe I am wrong or not or its just me.

But good point with the savings. I am trying to do this with my colleagues on my blog.

Thank you.