Have you stopped studying but still living like a college student? No worries. Living like a college student may just be what you need to impact your financial future.

When you’ve finished college, the best thing about landing your first job is that you finally have sufficient money to do things. Wow, enough money to do anything you want. You are no longer living like a poor college student, you’re an adult now.

Wait, let me stop you right there. Maybe it isn’t so bad to keep living like a college student for a couple of extra years.

When you have landed your first job and you’re earning more money, that doesn’t mean that you should spend it all.

The Math Of Living Like A College Student

If you’re in college and you’re earning $20K per year from several jobs. You’re working super hard to pay for all your college expenses and you’re graduating college with $20K in student loan debt.

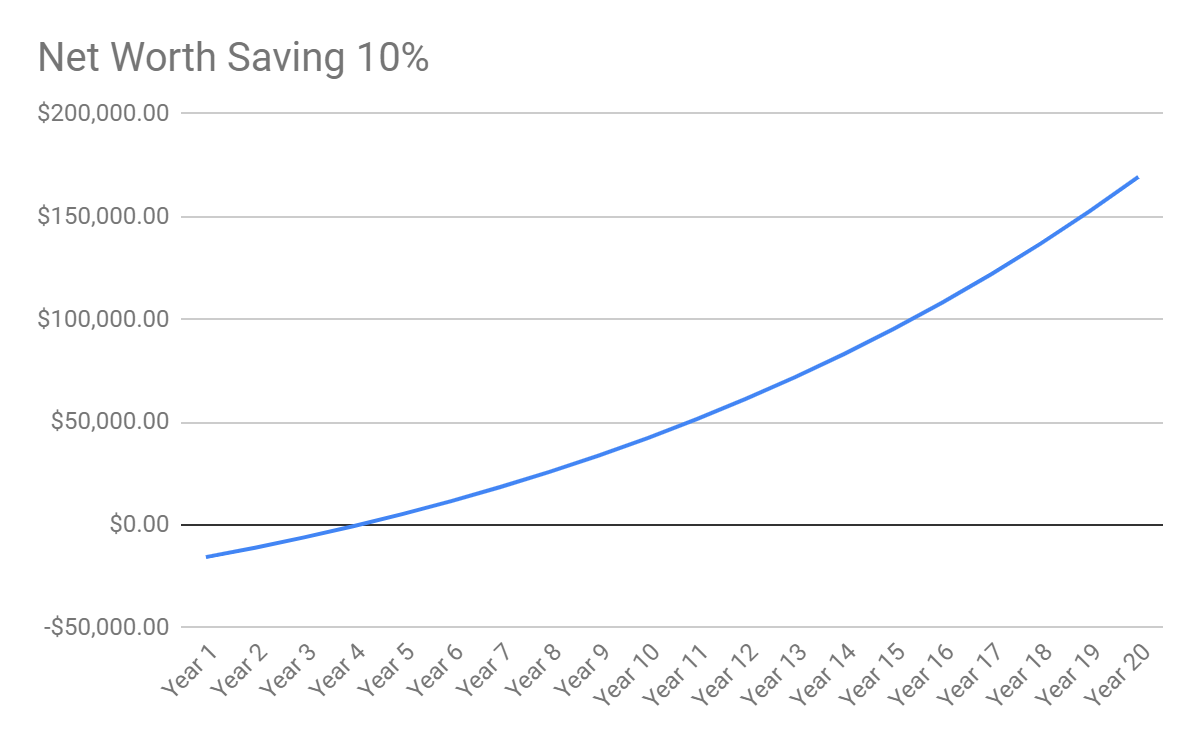

Saving 10% Per Year

You’re landing your first job and you’re earning a staggering $50K. You’re so proud of yourself that you want to get a brand new car and update it every 4 years. Besides that, you also update your living situation because you really enjoy having your own space. All of your friends have the same lifestyle, so you go out for dinner and drinks every weekend.

During the week you’re pretty good at saving money, so that’s something to be proud of. Because you’re much more aware of money than your peers, you still manage to save $5K per year. You try to keep the spending around the same amount because you want to retire early. Every year your salary increases by 3% and your spending increases by 3%. The invested amount grows at 5% per year.

This would be your net worth after 20 years:

When you’re saving 10% of your income per year, your net worth would be $169K after 20 years.

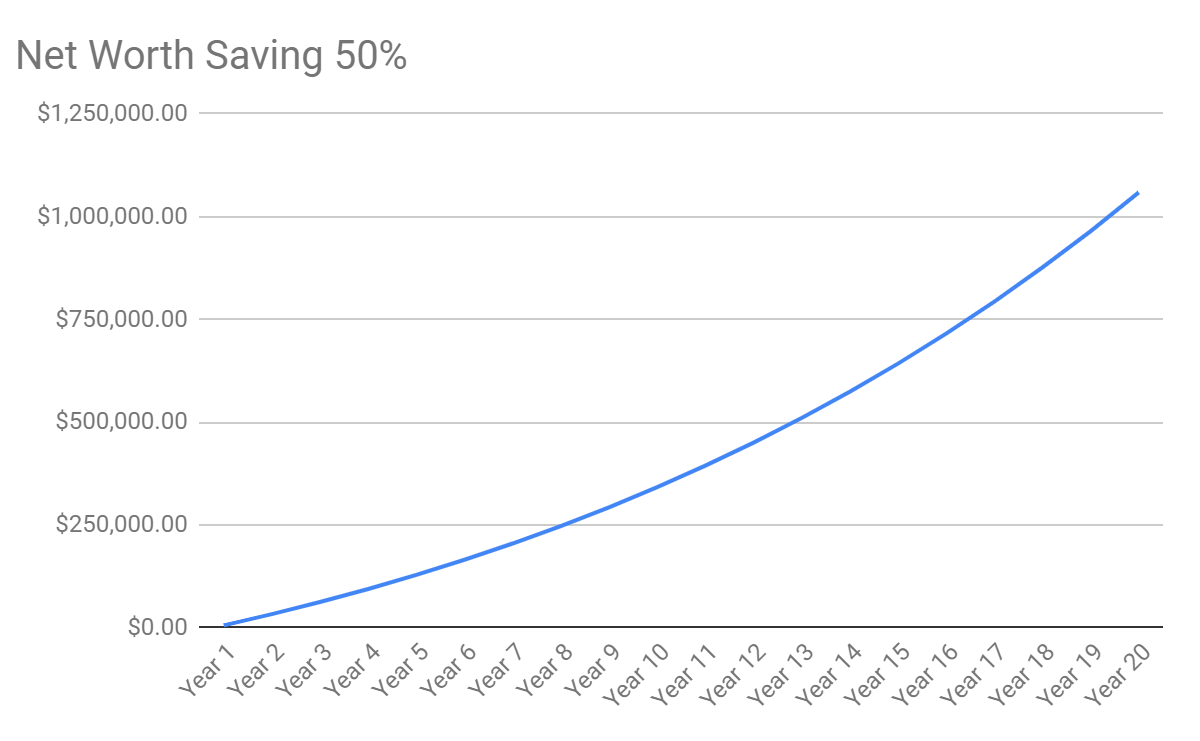

Saving 50% Per Year

When you’re landing your first job, you’re earning $50K. You try to keep your expenses to the same level as in college, but you can’t resist going out to eat a couple of times per week and you slightly upgrading your car. Besides that, you’re still saving $25K.

Both your salary and your expenses grow by 3% per year. Your invested amount grows a conservative 5% per year.

So the numbers are:

- Salary $50K, 3% yearly growth

- Spending $25K, 3% yearly growth

- Your invested portfolio is appreciating with a 5% return per year

The net worth after 20 years would be:

Your net worth after 20 years when you’re saving 50% of your income per year would be $1,059K. Meaning it would be over $1 million!

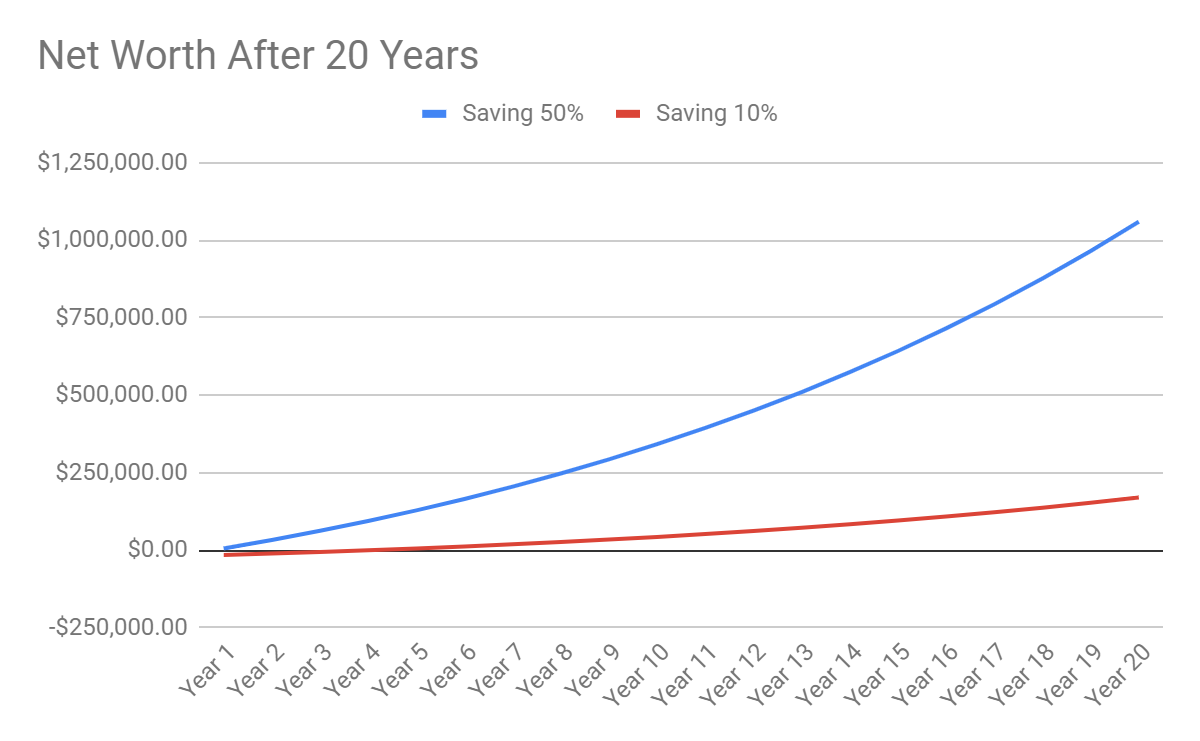

If we compare the two together in a graph, you can see how they perform here:

This is a huge difference because of one simple decision: living like a college student. When you have just started working and you’re getting used to some of the luxuries in life like a new car or going out to eat multiple times each week.

When you’ve set the tone early in your working career, compound interest can work its magic over more money. Just because you start early and you let time take care of your investments.

How I Avoid Overspending

When I was in college, there was definitely no room for overspending. I would try and save as much as possible for fun things I really enjoyed doing, like making trips and studying abroad. This made sure that I kept my other spending in check.

When you have finished college and started getting your first paycheck, I remember the feeling of having so much money in my account. It was amazing! I felt like I could buy everything I wanted, which I did for a couple of months.

I went to eat out more, went on more trips to visit friends, and spent more on groceries. After a couple of months, I noticed I was inflating my lifestyle and I decided to cut back on it.

No regular eating out anymore, visiting friends a couple of times per month rather than every weekend, and getting my grocery bill below $70 monthly.

Looking back, I even may have looked into alternatives to college, to not go studying in a traditional school.

My Major Savings Categories

The major thing I do to save money every month is to live in a small apartment, have no car available anymore, and keep my other spending in check.

When I first started working, I needed an apartment fast. I was driving 2 hours one way to work and I was sick of it within one week. I settled for a student apartment with 3 housemates, which were all ending their studies or started working. This was a good deal, for less than $300 per month including utilities.

This is what really set me up for success. If I were to live alone for that 1.5 years that I lived there, I would surely have spent triple. Studios or a small apartment for yourself are around $900 per month.

Besides that, I got a lease car from the company when I started working there. In the Netherlands, the government sees your lease car as extra income. If you drive your leased car privately, you need to pay extra for that on your payslip.

The thing is that once you drive your car privately, you can’t just stop it in the middle of the year. Meaning that for the entire of 2019, I got less salary because of this. In 2020 I decided that I will not drive my car privately anymore and I will not pay this extra amount since I am barely using it.

From April 1st, when I start my new job, I will not have a car at all. The office is in Amsterdam and the parking fees are incredible there, so I will go there by public transport.

If this is not possible in your situation, I would suggest you buy a used car instead of a fancy new car to keep the costs down. It will be less fun, but it will also cost a lot less.

Those two are my major savings categories at this moment. I also track all my other spending, where I will correct if I’m overspending on a category consistently. There is no need to be too strict about the budget and feel like you’re restricting yourself. You can live have a fun frugal life all at the same time.

How I Avoid Feeling Like I’m Missing Out

If you’re having a budget and you feel like you’re restricting yourself, this is not the way to keep yourself motivated. You should feel like you’re spending on things that make sense to you and that give you joy.

You can do that by focusing on your joy. What spending makes you happy? How do you want to spend your money?

I spend a lot of money on things that make me happy, like travel and festivals. But I will brutally cut back on things that I do not care about, like eating out and cars.

Because I am spending money that aligns with my priorities, I don’t feel like I’m cutting back or restricting myself in any way. If you feel like that, revise your budget so that you focus on the things that give you joy.

I feel that my money gives me options, which is worth a lot for me. I can say to my employer that I want to go on a four-month mini-retirement, I can keep my job, and go. Do whatever I want in my mini-retirement.

Also, I can contribute over half my income to my savings, investing, and peer-to-peer lending.

When I look at my friends, I don’t feel like I’m having any less quality of life. Many of my friends are graduated from university and have a stable financial foundation. Some have some more student loans than others, but they’ll get there.

Set Yourself Up Financially Successful

It is hard to deflate your lifestyle once you have increased your cost of living. A nice home, fancy cars, and eating out more is something that you will get used to very quickly. If you never inflate it, there is absolutely no reason for deflation.

If you start with building up your financial habits right when you’re out of university and still working your weekend jobs, it’s easier to stick to all of it. When you’re going for your financial goals, it is more important to look ahead than to overspend and need to look back all the time.

Basically, you’re paying for your lifestyle a few years ago when you go into debt. That’s not what will get you ahead financially.

It is important to start making your retirement a priority. Start building up your retirement accounts as soon as you can. This is important to let your income grow as much as possible. Time in the market > timing the market.

Focus on what you want financially and go for it. Whether that is building up your emergency fund, going on your dream vacation, or working towards financial independence.

If you are taking your time to build up these financial habits and stick to living like a college student for a few more years, you can hit the ground running. Take the time to have good financial habits now and get the life you want.

Are you living like a college student?

Like this post? Save it for later! ????

Founder of Spark Nomad, Radical FIRE, Journalist

Expertise: Personal finance and travel content

Education: Bachelor of Economics at Radboud University, Master in Finance at Radboud University, Minor in Economics at Chapman University.

Over 200 articles, essays, and short stories published across the web.

Experience: Marjolein is a journalist and founder of Radical FIRE, a personal finance platform, and Spark Nomad, a travel platform. Marjolein has a finance and economics background with a master’s in Finance. She has quit her job to travel the world, documenting her travels on Spark Nomad to help people plan their travels. Marjolein has written for publications like MSN, Associated Press, CNBC, Town News syndicate, and more.

Thanks for stopping by Steveark! Regarding the car, I was paying €150 per month in additional taxes which included everything you mentioned. That’s a lot cheaper than owning a car yourself. I guess it depends on how much you use the car. When you’re using it a lot and you would have a car anyways, it can be a huge saving factor as you mention. For me personally I am not using it at all now and I would not have bought a car myself, so it would be €150 spent instead of money saved. I’m happy that in your case your company car saved you a lot of money, that’s awesome!

I agree with your advice but when it came to having a free company car that was worth a lot to me. I had unlimited personal use plus free gas. I did pay tax on the personal usage but tax rates are pretty low compared to paying for a car and gas yourself. Plus all the maintenance, oil changes, tires etc were free and they replaced the car with another brand new one every few years.